2025 Recap: Five Defining Developments That Reshaped the Market

Rather than being defined by a single shock or crisis, 2025 was shaped by a series of gradual but important changes in how markets functioned. Conditions that supported strong asset performance in prior years — abundant liquidity, coordinated central bank policy, and reliable dip-buying — began to fade.

Markets did not move abruptly from strength to weakness. Instead, support became less consistent, volatility increased, and performance became more uneven. These developments signaled a shift toward a later stage of the cycle, where selectivity, risk management, and fundamentals mattered more than broad market momentum. The five factors that follow highlight how this transition unfolded.

Global Macro: The End of Synchronized Liquidity Expansion

The defining macro development of 2025 was not a single policy decision, crisis, or headline event. It was the quiet but decisive end of synchronized global liquidity expansion. The era following COVID was characterized by an extraordinary degree of coordination. Central banks moved together, liquidity surged together, and risk assets rose together. That regime ended in stages — and 2025 was the year the divergence became impossible to ignore.

Rather than moving in unison, central banks began responding to their own domestic variables. The Federal Reserve faced the tension between inflation control and financial stability. The ECB navigated uneven growth across member states. Emerging markets remained constrained by currency stability and capital flows.

Bank of Japan has increased rates to the highest level since the ‘90s

Most notably, Japan began signaling an exit from its long-standing ultra-loose stance. Even incremental normalization in Japan carried outsized global consequences due to its role as a funding anchor for risk-taking worldwide. As Japanese policy shifted, the yen carry trade — long a silent enabler of global leverage — began to unwind.

As funding costs rose and volatility returned, leveraged positions across asset classes were quietly reduced. For crypto, this mattered deeply. Crypto has historically thrived when global funding is cheap and abundant. As carry trades reversed and leverage contracted, crypto became more sensitive to global risk repricing rather than insulated from it.

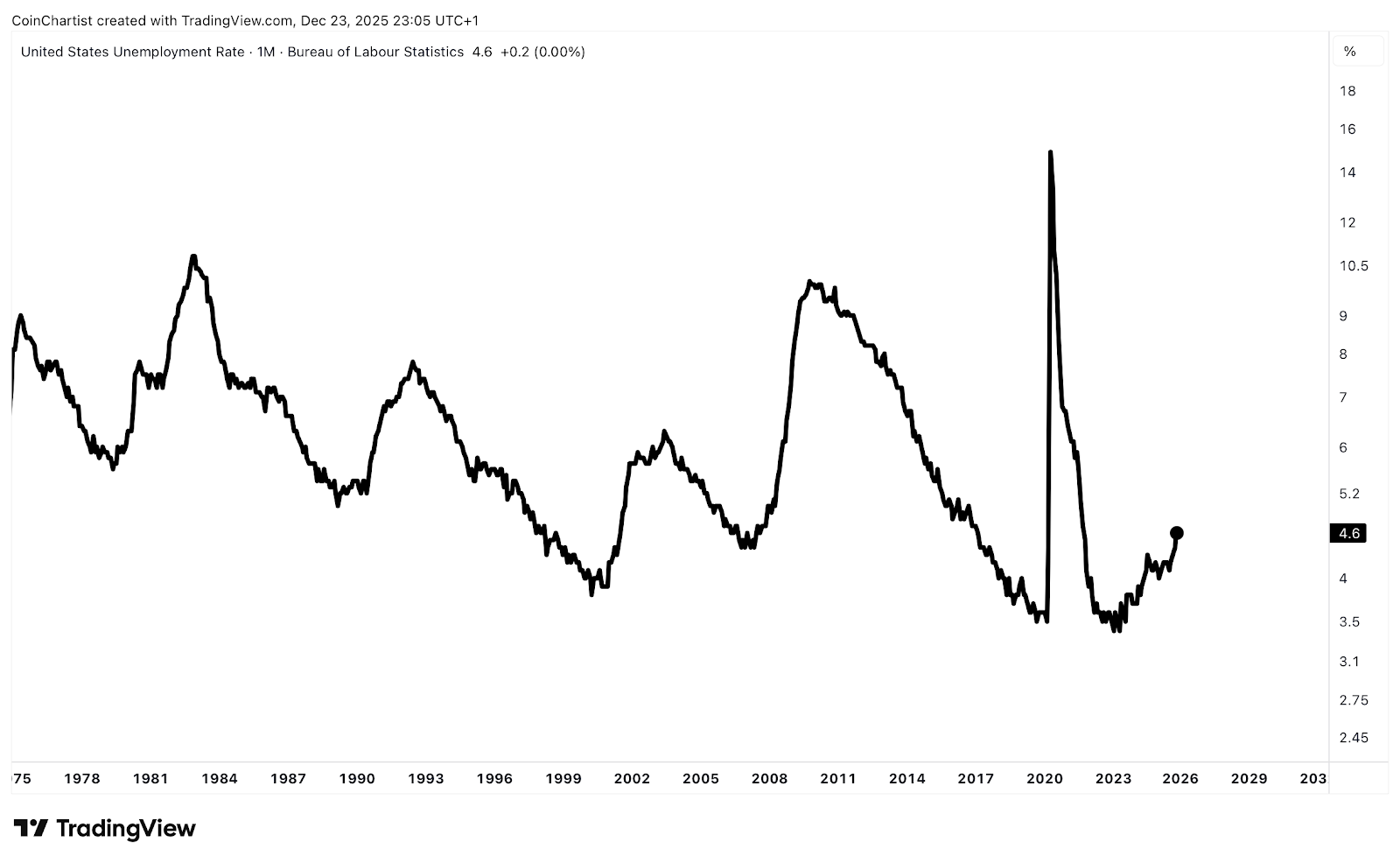

Macro Cross-Currents: Recession Signals vs Asset Inflation

One of the most confusing aspects of 2025 was the coexistence of weakening economic indicators and resilient asset prices. Labor markets began to soften. Forward-looking growth indicators rolled over. Business investment slowed. These signals pointed toward economic deceleration, not acceleration. Yet markets initially treated these developments as temporary or even bullish, assuming policy accommodation would arrive quickly.

Asset prices often reflect past liquidity conditions rather than current ones. The strength observed in early and mid-2025 was largely a function of prior stimulus, delayed capital deployment, and structural demand created earlier in the cycle. This created the illusion of economic resilience even as underlying conditions weakened.

Employment rates are often a recession signal

Markets remained elevated because positioning was crowded, narratives were entrenched, and policy expectations were optimistic. Investors anchored to previous playbooks: slowdowns would be met with easing; easing would reflate assets. What changed was timing. Policy relief did not arrive as quickly or as broadly as markets expected.

Crypto, sitting at the intersection of liquidity and sentiment, reacted sharply once the disconnect closed. When expectations reset, price adjustments occurred rapidly. The speed of repricing reflected not panic, but the sudden removal of misplaced confidence.

Bitcoin: From Institutional Acceptance to Maturity

Bitcoin’s evolution in 2025 was not defined by retail enthusiasm or narrative momentum. It was defined by institutional adoption colliding with long-term holder distribution — a dynamic that reshaped how Bitcoin trades at scale. This was the year Bitcoin fully crossed from speculative asset into financial infrastructure.

The introduction and normalization of spot Bitcoin ETFs fundamentally altered Bitcoin’s demand profile. Institutional capital began to arrive consistently, predictably, and in size. Pension funds, wealth managers, family offices, and corporate treasuries gained exposure not through cycles of enthusiasm, but through allocation frameworks.

Unlike prior cycles where new buyers chased momentum, ETF-driven demand behaved more like steady accumulation, absorbing supply without amplifying price velocity. This shift made Bitcoin more stable and less explosive.

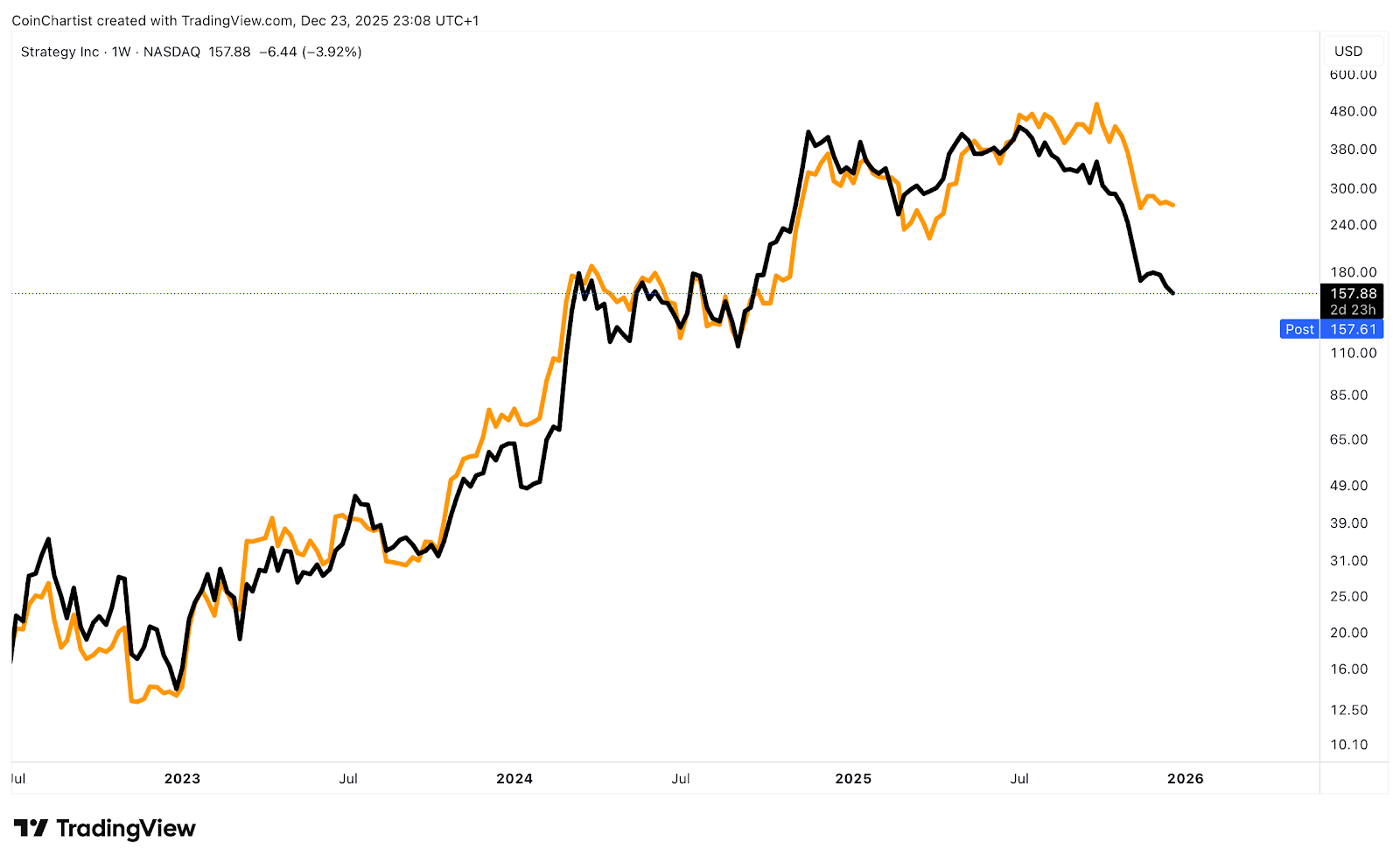

Another defining feature of 2025 was the rise of Bitcoin treasury companies treating BTC as a strategic reserve asset rather than a speculative holding. Firms like Strategy (formerly MicroStrategy) continued to expand their Bitcoin exposure, reinforcing the thesis of Bitcoin as long-duration, non-sovereign collateral.

Bitcoin (orange) versus MSTR (black)

This trend signaled growing confidence in Bitcoin’s survivability and relevance. But it also concentrated ownership among entities with long-term horizons, reducing the frequency of panic selling while increasing sensitivity to macro liquidity conditions.

When Bitcoin reached new all-time highs above $100,000, the psychological tone was markedly different from prior cycle peaks. There was no broad euphoria. No parabolic retail frenzy. Instead, the move felt measured, almost restrained. This high represented acceptance, not mania. Bitcoin was proving it could exist at six-figure prices within a regulated, institutional framework.

While institutions pushed Bitcoin above $100,000, long-term holders — often referred to as “OG whales” –– finally decided to start cashing in their coins. Many of these participants accumulated Bitcoin well below current prices and used strength above $100,000 as an opportunity to realize gains.

This selling pressure did not signal a loss of confidence. It represented generational wealth transfer within the ecosystem. Importantly, this supply was largely absorbed by institutional buyers. The result was a market where sell pressure and buy pressure largely offset, capping upside while establishing a higher structural price floor.

Altcoins: Narrative Saturation and Capital Exhaustion

While Bitcoin matured, the altcoin market struggled under its own weight. Narratives were abundant, but capital was finite. Innovation did not translate into performance because liquidity could not support thousands of simultaneous altcoins competing for the same market share.

The broad assumption that all assets would rise together no longer held. Capital became selective. Most altcoins were left behind. Each new narrative generated less incremental capital than the last. Market participants became desensitized.

The crypto market entered 2025 with thousands of tradable tokens, many offering marginal differentiation and minimal real-world utility. Capital simply could not support this breadth.

Altcoins (OTHERS) failed to make a meaningful higher high

Unlike Bitcoin, spot altcoin ETF launches failed to meaningfully move markets. Expectations that Ethereum or other large-cap altcoins would benefit from similar institutional inflows proved optimistic.

Meme coins captured attention and short-term speculation, but they did not lead the market. Instead, they functioned as liquidity traps, drawing capital away from productive assets and amplifying volatility without creating lasting value. Their prevalence was not a sign of market health — it was a symptom of speculative exhaustion.

Market Structure & Psychology: From Complacency to Fear

The most important shift of 2025 was psychological. It did not arrive with headlines — it arrived with behavior. The October 10 flash crash marked a turning point. Record-breaking liquidations occurred rapidly across crypto markets, catching both retail and institutions off guard.

More important than the price action was the psychological response. Confidence was destroyed. The assumption that dips would be bought reflexively broke down. For the first time in the cycle, market participants were forced to confront the possibility that a bear market without a more familiar altcoin season was not just theoretical, but plausible.

Volatility re-emerged as a signal of regime change. Rather than being suppressed by liquidity, volatility reflected uncertainty, repositioning, and risk reduction. Markets were no longer trending — they were searching for direction and confidence.

The October 10 bloodbath left massive wicks on crypto charts

Retail participation declined sharply. Institutions did not exit, but they became highly selective. Capital shifted toward assets perceived as durable rather than exciting. As crypto volatility increased, capital quietly rotated into traditional hedges. Gold and silver attracted renewed interest as stores of value during macro uncertainty. This did not represent a rejection of crypto — it represented risk diversification.

By year-end, capital preservation had replaced growth maximization as the dominant objective. This shift was subtle but decisive. Assets began sorting themselves by credibility, liquidity, and durability. The market quietly began ranking what mattered — and what did not.

Summary

Overall, 2025 marked a transition rather than a turning point. Liquidity did not disappear, but it became less predictable. Bitcoin continued to gain acceptance as a longer-term asset held by institutions, while many altcoins struggled as capital became more selective.

Market behavior reflected this change. Volatility increased, investors became more cautious, and interest grew in assets viewed as more stable, including traditional hedges. By the end of the year, markets were less driven by excitement and more influenced by risk awareness and positioning.

These shifts helped set clearer expectations heading into 2026. While opportunities remain, the environment now favors patience, diversification, and a greater focus on durability than in earlier phases of the cycle.

Suggested Posts

YouHodler is regulated in Switzerland, the EU and Argentina.

YouHodler SA

Registered financial intermediary

YouHodler Italy S.R.L.

Registered as a VASP with the OAM

YouHodler SA

Registered as VASP with Banco de España

YouHodler SA Branch in Argentina.

Registered as a VASP with the CNV.